Retirement income planning is about more than generating cash flow.

It is also about understanding where that income comes from.

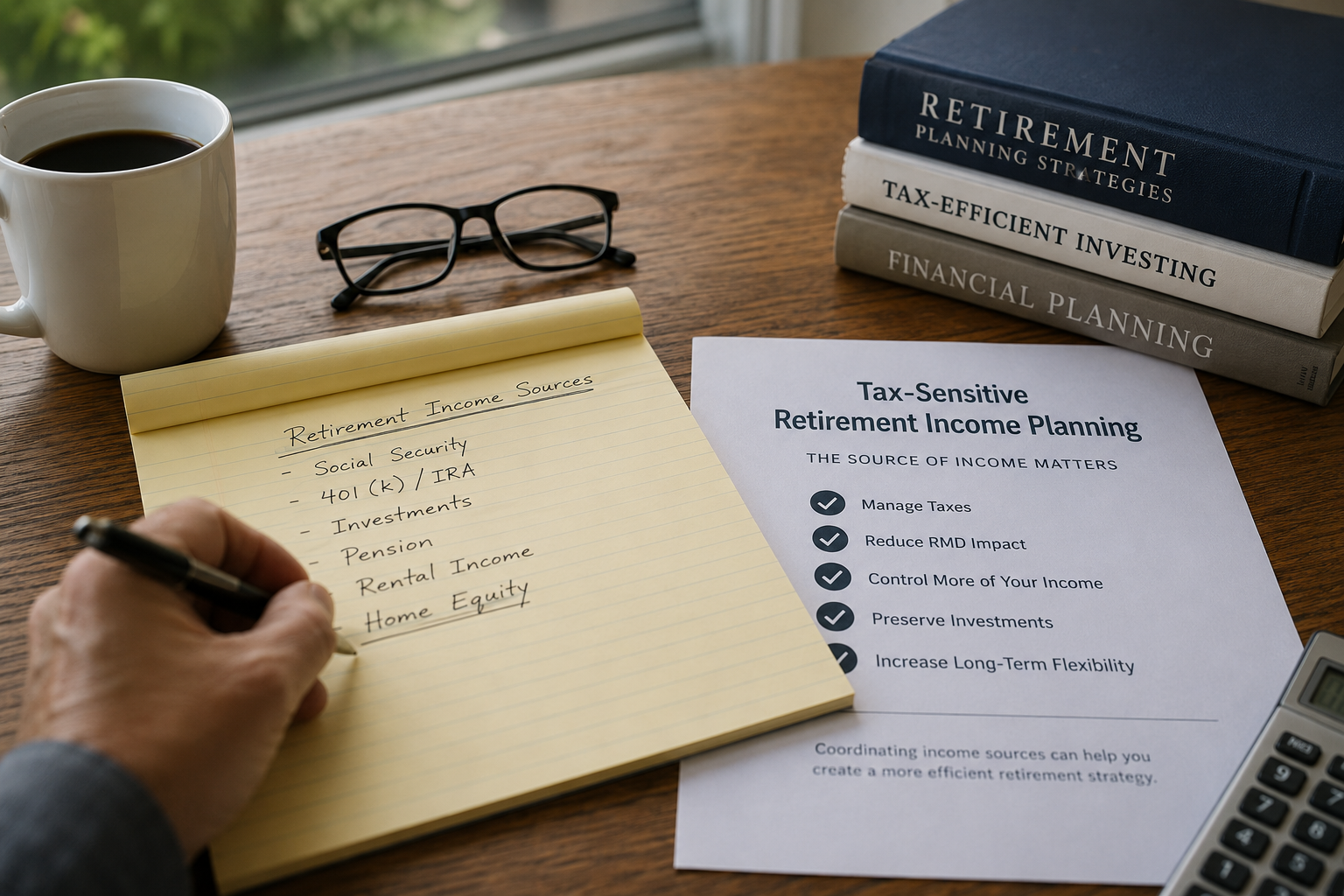

For many retirees, income may be generated from multiple sources, including:

- Social Security benefits

- Traditional IRAs

- 401(k) plans

- Roth accounts

- Taxable investment accounts

- Pensions

- Cash reserves

- Housing wealth

Each income source may have different tax implications.

As a result, many financial advisors focus not only on how much income a retiree needs, but also on how that income is sourced throughout retirement.

Housing wealth is often one of the largest assets on a retiree’s balance sheet, yet it is frequently overlooked in retirement income discussions.

As retirement planning continues to evolve, many advisors are taking a broader view of the resources available to clients and evaluating how those resources may work together to support long-term retirement goals.

Retirement Planning Has Become More Tax-Aware

Today’s retirees face a more complex planning environment than previous generations.

Many retirees are balancing:

- Required Minimum Distributions (RMDs)

- Social Security income

- Investment withdrawals

- Capital gains considerations

- Medicare premium thresholds

- Legacy planning goals

As a result, advisors are increasingly focused on tax-sensitive retirement income planning.

The goal is not simply generating income.

The goal is generating income efficiently while preserving flexibility.

Why Income Sources Matter

Consider two retirees who both need an additional $25,000 per year.

The amount is identical.

The source of the income may not be.

One retiree may choose to withdraw funds from a retirement account.

Another may utilize cash reserves.

A third may draw from taxable investments.

Each approach may create different planning outcomes.

This is why many advisors spend significant time evaluating withdrawal sequencing and retirement income coordination.

The conversation is often less about how much money is available and more about which resources may be most appropriate to use at a given time.

Housing Wealth Is Often Missing From the Conversation

For many retirees, home equity represents one of the largest assets on the balance sheet.

Yet it is frequently excluded from retirement income planning discussions.

Historically, housing wealth has often been viewed primarily as a legacy asset or a resource to be accessed only as a last resort.

Today, many retirement professionals are taking a broader view.

The question is no longer simply:

“How much equity does the client have?”

The question may be:

“How does housing wealth fit into the overall retirement plan?”

Creating Additional Flexibility

One of the primary goals of retirement planning is maintaining flexibility.

Market conditions change.

Tax laws evolve.

Healthcare expenses arise.

Unexpected opportunities appear.

Having multiple sources of liquidity may help retirees and their advisors make more informed decisions.

For some retirees, a reverse mortgage may provide access to housing wealth that can serve as an additional planning resource.

Potential uses may include:

- Supplementing retirement cash flow

- Managing unexpected expenses

- Preserving investment assets

- Supporting aging-in-place goals

- Providing additional liquidity during market downturns

The objective is not necessarily to replace traditional retirement income sources.

The objective is to create more options.

Coordinating Multiple Retirement Assets

Financial advisors often seek to coordinate retirement assets rather than relying heavily on a single source of income.

This may involve evaluating:

- Investment portfolios

- Retirement accounts

- Social Security benefits

- Cash reserves

- Home equity

The most effective retirement plans are often those that consider the entire balance sheet.

Housing wealth may represent a meaningful component of that analysis.

A Collaborative Planning Conversation

Tax-sensitive retirement income planning should involve collaboration among trusted professionals.

This may include:

- Financial advisors

- Tax professionals

- Estate planning attorneys

- Retirement planners

- Reverse mortgage specialists

Each professional brings a unique perspective to the planning process.

Housing wealth should be evaluated alongside other retirement assets as part of a comprehensive planning discussion.

Looking Beyond Traditional Retirement Income Sources

Retirement planning continues to evolve.

Today’s retirees have more financial tools, more planning opportunities, and more complexity than ever before.

As advisors seek to build flexible retirement income strategies, housing wealth may deserve greater attention.

Not because it is the right solution for every client.

But because it may represent an important resource that is often overlooked.

Final Thought

Tax-sensitive retirement income planning is ultimately about flexibility.

It is about understanding the various resources available to retirees and thoughtfully coordinating those resources over time.

Housing wealth deserves a seat at the retirement planning table.

Not as a replacement for traditional strategies.

But as another potential resource that may help retirees navigate retirement with greater confidence, liquidity, and flexibility.

The strongest retirement plans often come from evaluating the entire balance sheet—not just the assets that are traditionally discussed.

Additional Resources

- Morningstar Retirement Planning Resources — Research and insights on retirement income, withdrawal strategies, and portfolio management.

- Wade Pfau’s Retirement Researcher — Retirement income research focused on Social Security, housing wealth, retirement spending, and long-term financial planning.

Is Housing Wealth Right for Your Retirement Strategy?

Every retirement plan is unique, and using home equity isn’t the right solution for everyone. But for many homeowners age 55 and older, it can be an important tool for improving cash flow and increasing financial security.

Understanding how housing wealth fits into an overall retirement strategy can help you make more informed decisions about the future.

If you’d like to learn more about how a reverse mortgage may help strengthen your retirement plan or your client’s plan, we’re happy to walk you through the options.

Send us a note below to request more information.

About the Author

Rick Rodriguez, CRMP®, is Director of VIP Mortgage Reverse and has specialized in reverse mortgages since 2004. Recognized as one of the leading reverse mortgage professionals in the country, Rick works closely with retirees, financial advisors, real estate professionals, and other trusted advisors to help evaluate how housing wealth may fit within a comprehensive retirement plan.

As the first Certified Reverse Mortgage Professional (CRMP®) in Southern Nevada, Rick is passionate about educating both consumers and professionals on the evolving role of home equity in retirement income planning. His writing focuses on retirement cash flow, housing wealth, Social Security strategies, portfolio preservation, and other planning concepts that can help retirees make more informed financial decisions.

Learn more at www.TheRetirementHomeLoan.com.

This material is for educational purposes only and is not intended as tax, legal, investment, or financial planning advice. Financial advisors should consult with appropriate professionals when evaluating strategies for individual clients. Reverse mortgage borrowers must meet program requirements and remain responsible for property taxes, homeowners insurance, home maintenance, and occupancy obligations.