Retirement Home Loan Articles

How Much Do You Need to Retire? Why Your Home May Be Part of the Answer

How Much Do You Need to Retire? Why Your Home May Be Part of the Answer Retirement planning has never been more challenging. A recent analysis from Investopedia estimates that […]

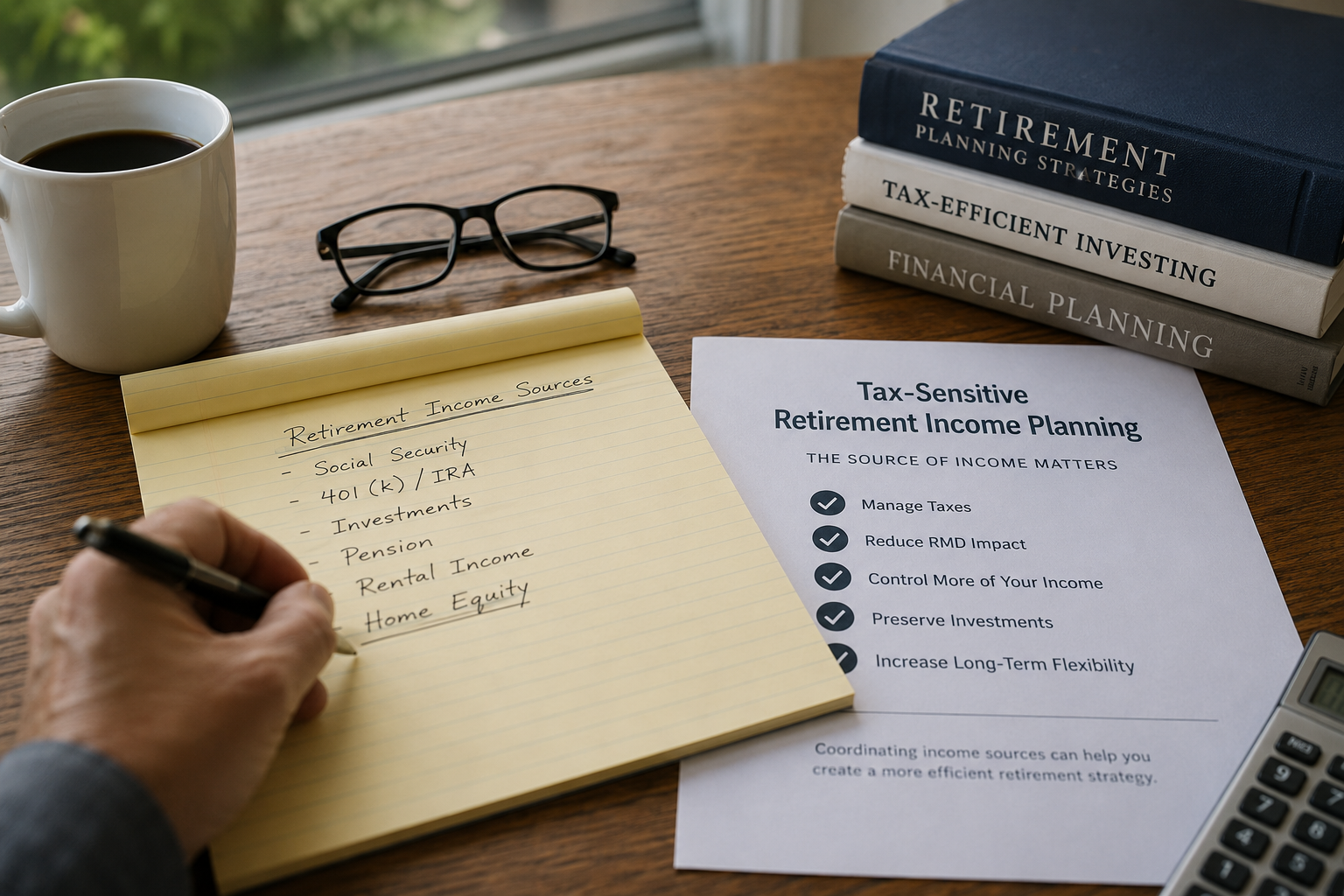

Tax-Sensitive Retirement Income Planning: Why the Source of Retirement Income Matters

Retirement income planning is about more than generating cash flow. It is also about understanding where that income comes from. For many retirees, income may be generated from multiple sources, […]

Aging in Place: How Housing Wealth and Technology Are Changing Long-Term Care Planning

For most retirees, the goal is simple: Stay independent. Stay comfortable. Stay at home for as long as possible. In fact, numerous studies have shown that most older adults prefer […]

Delaying Social Security and Portfolio Withdrawals: Could Housing Wealth Create More Retirement Income Flexibility?

Financial advisors spend significant time helping clients make important retirement income decisions. When should Social Security benefits begin? How much should be withdrawn from investment accounts? How can retirement […]

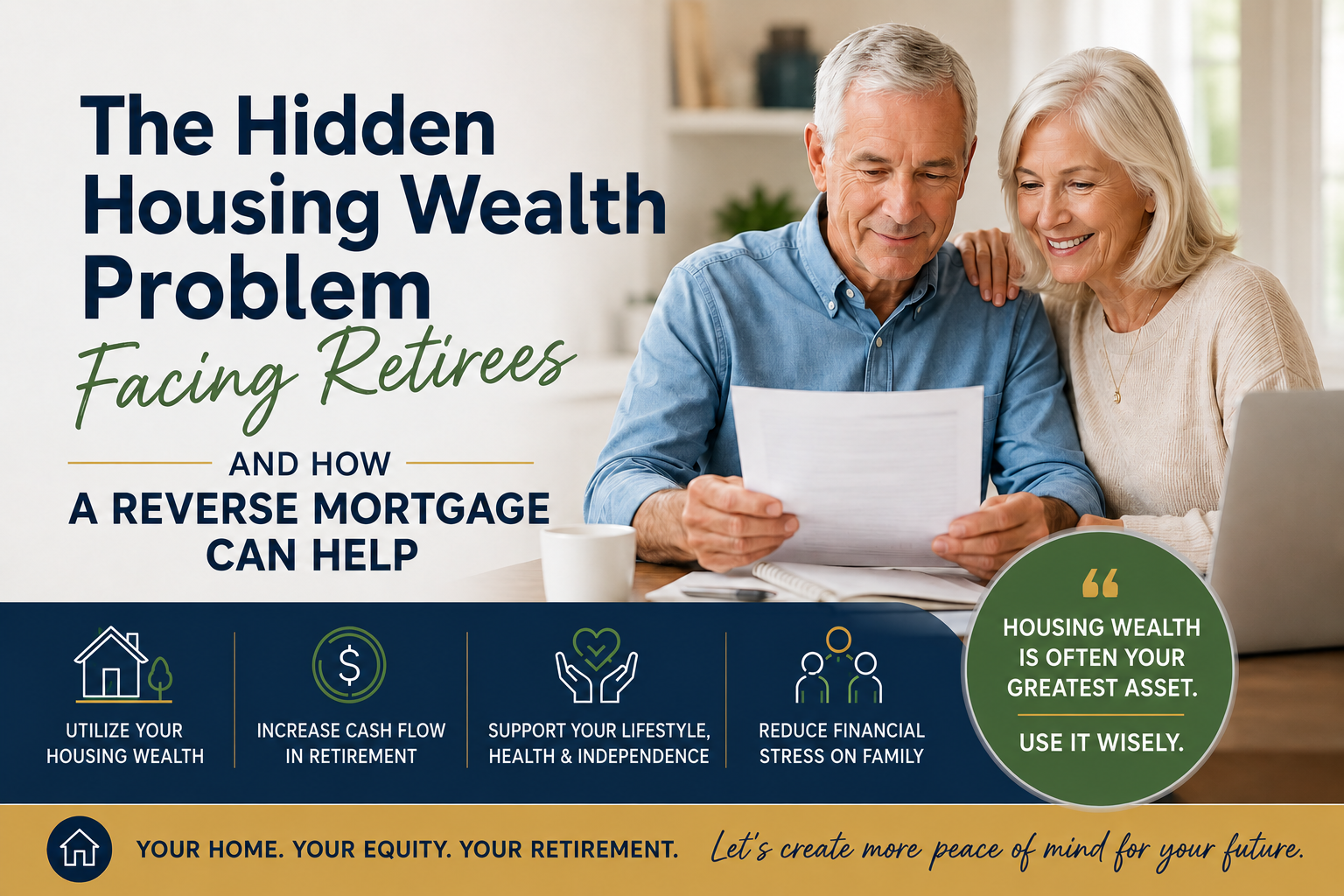

The Hidden Housing Wealth Problem Facing Retirees — And How a Reverse Mortgage Can Help

A recent Forbes article titled “The Great Wealth Transfer’s Hidden Housing Problem” highlighted an important issue many families are beginning to face across America. As trillions of dollars are expected […]

Retirement Cash Flow Planning: How Eliminating a Mortgage Payment May Improve Retirement Flexibility

For many retirees, retirement planning is not just about net worth. It is about monthly cash flow. A client may have substantial assets, significant home equity, and a well-structured investment […]

Sequence-of-Returns Risk: Why Financial Advisors Should Not Ignore Housing Wealth

One of the greatest risks in retirement planning is not simply market volatility. It is the timing of that volatility. Financial advisors understand this well. A retiree who experiences negative […]

Why “My Client Doesn’t Need a Reverse Mortgage” May Be the Wrong Analysis

Financial advisors are trained to look beyond surface-level answers. A client may not “need” a Roth conversion.They may not “need” tax-loss harvesting.They may not “need” a trust review.They may not […]

Reverse Mortgage Retirement Planning for 55+ Homeowners

A recent Realtor.com article highlighted a reality many families, real estate professionals, and financial advisors are seeing firsthand: the amount Americans believe they need to retire comfortably keeps moving higher. […]

Housing Wealth: The Third Leg of Retirement Income

The Third Leg of Retirement: When Social Security and Savings Aren’t Enough For decades, retirement planning has been described as a three-legged stool built on Social Security, pensions, and personal […]

How a Reverse Mortgage Can Work with Medicaid Planning

For many older homeowners, one of the biggest financial concerns is how to pay for long-term care while protecting their home and maintaining eligibility for Medicaid. What many people don’t […]

Senior Home Equity Reaches Record $14.66 Trillion — What It Means for Retirement Planning

Senior homeowners are sitting on more housing wealth than ever before. According to recent data reported by HousingWire, senior home equity surged to a record $14.66 trillion in the third […]

How A Reverse Mortgage Loan Could Help Protect You And Your Home In Uncertain Times

Can you protect something? Maybe your home?

Can you protect something? Maybe your home?

Can you protect something? Maybe your home?

Can you protect something? Maybe your home?Do you remember in 2008 what had happened before and after the housing market bubble? The market was going up, home values were increasing, and we had low unemployment rates before the bubble crashed. Before the crash, when houses in larger cities went up for sale, a few hours later, it would have multiple offers over the asking price. Then shortly after the housing bubble crashed, home values had started to drop, and the time frame for selling homes became much longer. After the bubble, the Home Affordable Refinance Program (HARP) became a popular loan option because a lot of people owed more on the mortgage than what they were worth from the home’s declining values.

Fast-forward to today, where you see more and more seniors continue to stay in their homes longer, and starter homes are getting harder and harder to find. Millennials are looking to buy starter homes, and the supply for entry-level homes is going down. Prices and demand for entry-level homes for the past few years have been significantly increasing.

Before Covid-19, the market was going up, home values were increasing, and we had low unemployment rates. According to thebalance.com, the unemployment rate for 2019 was at 3.5%, which the last time we had seen rates that low was since 1969 when Nixon took office and just before the mild 1969-1970 Recession. Do you believe history tends to repeat itself, and all ships rise or fall with the tide? Are you concerned about your home values going down just like the stock market has decreased recently?

There is a lot of worry and fear being caused currently from the Covid-19 virus in the news lately. For some, the market’s recent downswing of 30% in their retirement funds is causing even more fear. We are all hoping this will be a fast rebound like the 1969-70 mild recession, like a rubber band pulled back, testing its limits, and shooting forward with a stronger force behind it. Hopefully, it will not take several years, like the 2008 housing bubble, took to recover. The question is, what can you do about it, so you’re not just sitting and hoping things change. If your 62 or older with some equity in your home, you may have the ability to use a reverse mortgage loan.

Here are some reasons why I believe a reverse mortgage loan is going to become a popular loan option like the HARP loan was after the 2008 bubble.

1. Are their better places to pull your money from besides your 401k accounts?

There have been many studies done that show it’s better for your portfolio’s survivability if you pull the money from a growing reverse mortgage line of credit in market downswings than from your investments.

Are you currently using your home equity to potentially strengthen your portfolio? Are you presently pulling money out of investments? Wouldn’t it be beneficial to have the funds come out of another source of funds rather than what you have in the stock market now*? If not your home, where else are you going to get the funds to meet the cash flow you need? The interest rate on a reverse mortgage loan is pretty low right now. Wouldn’t you rather leverage your available assets than ignore them to prevent you from having to sell your investments?

2. Are you concerned about your home values going down?

A reverse mortgage loan is a non-recourse loan. The definition from Investopedia for Non–recourse debt is a type of loan secured by collateral, which is usually property. If the borrower defaults, the issuer can seize the collateral but cannot seek out the borrower for any further compensation, even if the collateral does not cover the full value of the defaulted amount.

So if you are concerned about home values going down as they did after the 2008 housing bubble a reverse mortgage loan would be a good loan to consider. If your home value drops, the lender is not able to request their funds back that they already borrowed you.

3. What could the benefits of having additional cash flow be?

One of the first things said about reverse mortgage loans in most advertisements is no monthly mortgage payments except for taxes, insurance, and maintenance. In times of fear and concern tend to be the best time to have additional cash flow. The best time to help people is highest when there is a need when people are struggling. You can use the additional cash flow to help your loved ones who may be struggling with recently becoming unemployed and struggling to keep up with life essentials as buying food. If home prices, the market, and other items continue to lower in price, you can use the additional cash flow to purchase things at discounted prices. Whatever the reason is, I’ve never heard anybody complain about having additional cash flow.

It’s often wise to take the time to learn something new, and it doesn’t pay to wait. Rick R. Rodriguez is your local Certified Reverse Mortgage Professional, CRMP, who has been specializing in reverse mortgages since 2005 and has first-hand experience with how reverse mortgages helped homeowners back in 2008 to help you navigate through our current conditions. Whether you are looking in Las Vegas for a reverse mortgage or beyond, contact our team for more information.

Interested to know the amount of money you could receive with a reverse mortgage?

Click on the button to open the form that will help us customize a quote for you.